Commercial banks are business enterprises that serve as financial intermediaries. Thus, they attract savings of the population, capital, and other available funds that are released in the course of economic activity, in order to provide them for use by other economic entities that are temporarily in need of additional funds.

To solve these problems, banks carry out banking operations. The main operations in this direction are operations called active and passive.

Necessary for attracting and concentrating capital as working capital. Active operations are aimed at placing attracted resources to make a profit. Passive operations of commercial banks are called operations to accumulate their own resources, which are necessary for conducting active operations (including credit).

The formation of bank resources occurs through attracting funds from the population in deposits, issuing bank securities, obtaining loans from third-party banks and other operations that lead to an increase in the funds available to the banking institution.

Passive operations of commercial banks include accepting deposits; issuance of bank securities (bills, bonds, savings, maintaining accounts of various clients, including correspondent banks; receiving, including centralized credit resources; eurocurrency loans.

Commercial banks are specific institutions that, on the one hand, accumulate temporarily free monetary resources, and on the other hand, provide the funds they have available to enterprises and the population in need of resources for temporary use for a certain fee.

Passive operations of commercial banks determine the size of banking resources and, accordingly, determine the possible scale of their activities. In passive operations, funds are concentrated on passive or bank accounts. Passive transactions help banks acquire credit resources on the free market.

There are four main forms of passive operations: deductions from one’s own profits to increase or form funds; primary issue of bank securities (contributions to the authorized capital); obtaining loans from other legal entities; deposit operations (raising customer funds).

Passive operations of a commercial bank mediate the attraction of money that is already in circulation. First of all, passive operations include deposit operations to attract funds from legal entities and citizens into deposits, either time-sensitive or on demand. This is what constitutes the bulk of the bank's liabilities.

Time deposits are determined by the terms specified in the agreement. Such deposits pay a higher interest rate than demand deposits. The latter represent funds in accounts that are associated with settlements and demand deposits.

Actively passive operations of commercial banks are called commission, intermediary operations that banks perform on behalf of clients for a fee - a commission. These operations are called services. There are settlement services for domestic and international payments; trust services, which involve the bank’s purchase and sale of foreign currency, securities, and precious metals on behalf of clients; intermediation in the placement of bonds and shares; consulting and accounting services for clients, etc.

Acts primarily as specific credit institutions, which, on the one hand, attract temporarily free funds of the economy; on the other hand, using these raised funds, they satisfy the various financial needs of enterprises, organizations and the population.

The economic basis of the bank's operations for the accumulation and placement of credit resources is the movement of funds as an objective process that influences the formation and use of loaned values. By organizing this process, a commercial bank acts as a commercial enterprise that provides profitable placement of accumulated credit resources.

The operations of a commercial bank represent a concrete manifestation of banking functions in practice. The concept of “banking operations” is one of the fundamental ones, since it is the implementation of such operations by a legal entity that allows it to be classified as a credit institution and distinguished from other commercial legal entities operating on the basis of a license from the Central Bank of the Russian Federation (audit firms). In addition, carrying out such operations necessarily requires a license from the Central Bank of the Russian Federation.

Bank operations- these are transactions the object of which may be money, securities, precious metals and natural precious stones, systematically carried out by credit institutions and the Bank of Russia (its institutions) in accordance with the principle of exclusive legal capacity on the basis of:

· for credit organizations - the Law on Banks and the license of the Bank of Russia to carry out banking operations;

· for the Bank of Russia (its institutions) - the Law on the Bank of Russia

Banking service- this is a comprehensive activity of the bank to create optimal conditions for attracting temporarily free resources and to meet the needs of the client during banking operations, aimed at making a profit. In addition, the services of commercial banks can be defined as conducting banking operations on behalf of a client in favor of the latter for a fee.

The main characteristics of banking services include:

· intangible essence of services;

· the product is not stored, but banks create reserves of funds that are managed by the banker;

· banking operations and services are regulated by law;

· the sales system (provision of banking operations and services) is exclusive and integrated, since all branches of one bank perform the same set of banking operations and services.

It is important to note that, in accordance with Russian banking legislation, credit institutions are prohibited from entering into agreements and carrying out concerted actions aimed at monopolizing the banking services market, as well as limiting competition in banking. The acquisition of shares (stakes) in the authorized capital of credit institutions, as well as the conclusion of agreements providing for control over the activities of credit institutions (their associations), should not contradict antimonopoly rules.

In a market economy, all operations of a commercial bank can be divided into three main groups:

· passive operations (raising funds);

· active operations (placement of funds);

· active-passive (intermediary, trust, etc.) operations (Fig. 1.2).

Rice. 1.2. Structure of the main operations of a commercial bank

In Russian banking practice, the operations of commercial banks are also divided into three groups.

1. Passive Operations - operations to attract funds to banks and generate the latter’s resources.

Innovative financing and lending;

Equity participation with bank funds in the economic activities of enterprises;

Loans provided to other banks.

The bank’s active operations according to economic content are divided into:

· loan (accounting and loan);

· settlement;

· cash;

· investment and stock;

· warranty.

As a result of the implementation of active operations, bank assets are formed. Commercial bank assets can be divided into 4 categories:

· cash and equivalent funds;

· investments in securities;

· buildings and equipment.

Bank assets are divided on:

1. Highly liquid assets (cash, funds in accounts with the Central Bank, domestic foreign currency bonds);

2. Liquid assets (loans up to 30 days);

3. Long-term liquidity assets with a maturity period of more than 30 days, guarantees and sureties - a validity period of more than a year.

4. Low-liquid assets - buildings, structures.

Interest-bearing assets:

1) commercial loans to legal entities;

2) commercial loans to individuals;

3) short-term loans and deposits in banks;

4) short-term investments (in securities).

Non-income generating assets:

1. Cash;

2. Correspondent accounts;

3. Reserves in the Central Bank of the Russian Federation;

4. Interest-free loans, as well as overdue loans for which no interest is paid;

5. Capital investments.

By passive we mean such operations of banks, as a result of which there is an increase in funds held in passive accounts or active-passive accounts in terms of the excess of liabilities over assets.

Passive operations play an important role for commercial banks. It is with their help that banks acquire credit resources in the money markets.

There are 4 forms of passive operations of commercial banks:

a) primary issue of securities;

b) deductions from the bank’s profits for the formation or increase of funds;

c) loans and borrowings received from other legal entities;

d) deposit operations.

Passive operations allow banks to attract funds already in circulation. New resources are created by the banking system as a result of active credit operations. With the help of the first two forms of passive operations (a, b), the first large group of credit resources is created - own resources. The next two forms (c, d) of passive operations create the second large group of resources - borrowed, or attracted, credit resources.

Raised funds from banks cover over 90% of the total need for monetary resources to carry out active operations, primarily credit. Their role is extremely high. By mobilizing temporarily free funds of legal entities and individuals in the credit market, commercial banks use them to satisfy the national economy’s need for additional working capital, facilitate the transformation of money into capital, and meet the population’s needs for consumer credit.

Control questions

Passive operations.

Passive operations of a commercial bank- this is the activity of the bank to accumulate its own and borrowed funds for the purpose of their placement.

The purpose of commercial bank operations is as follows:

providing resources for the bank's activities;

formation of additional sources of funds for productive use in the economy;

increasing the income of individuals and legal entities receiving bank interest on deposits;

growth of the bank's equity capital;

creation of reserve funds for insurance of banking operations.

Passive Operations- operations to mobilize funds, namely: attracting loans, deposits (deposits, savings), obtaining loans from other banks, issuing own securities. Funds received as a result of passive operations are the basis of direct banking activities. Active operations - operations for placing funds. As a result of active operations, banks receive debit interest, which should be higher than the credit interest paid by the bank on passive operations. The difference between debit and credit interest (margin) is one of the most important traditional items of bank income (bank profit is also formed through commission fees for banking services).

Main passive operations of a commercial bank - deposit.

Deposit operations- These are fixed-term and permanent investments of bank clients. Funds held in demand accounts (demand deposits) are intended for making current payments - in cash or through a bank using checks, credit cards or letters of credit. Another type of deposits is time deposits (with certain maturities). These deposits usually pay higher interest depending on the term of the deposit, since banks can manage the depositor's funds for a longer period of time and have the opportunity to reinvest them. Most often, funds for a specific purpose are placed in urgent accounts, for example, amounts intended by an entrepreneur to purchase equipment in 6 months.

Passive transactions also include various savings transactions. Savings deposits serve to accumulate client funds, of which the client is issued a certificate (savings book).

Also, passive operations of a commercial bank include:

- creation and increase of equity capital through deductions from profits;

- issue of securities and their placement on the open market;

- deposit operations;

- interbank loans on the domestic and foreign markets.

Among deposit operations the following groups are distinguished:

¾ demand deposits;

¾ time and savings deposits.

Active operations.

These are operations to place borrowed and own funds of a commercial bank in order to generate income and create conditions for conducting banking operations.

Active operations of a commercial bank- these are primarily credit operations, investment operations, operations for the formation of bank property, cash settlement operations, commission and intermediary operations (factoring, leasing, forfaiting, etc.). All credit transactions can be grouped as follows (Fig.):

Active operations of banks- these are operations for issuing (placing) various types of loans. The most common type of credit issued by banks is a short-term loan to economic agents, usually to finance the purchase of inventories. This loan can be issued with or without actual collateral, but in any case, in order to obtain it, it is necessary to have reported financial documents characterizing the financial position of the borrower, so that the bank can at any time assess the likelihood of timely repayment of the loan.

Basic operations and role of commercial banks in a market economy. Money creation by the banking sector

The operations of commercial banks, which continue to play the role of “workhorses” in the modern banking system, can be divided into three main groups: passive (raising funds), active (placement of funds) and commission-intermediary and trust. Banks' resources consist of their own, borrowed and issued funds. Own funds (share and reserve capital and retained earnings) make up about 10% of the resources of a modern bank. The main part of them are funds raised in the form of deposits. Deposits are understood as both fixed-term and non-current (demand accounts) deposits of bank clients. Demand deposits are intended mainly for current payments; time deposits are made for longer periods. The bank can hold these deposits for a long time, increasing its interest income through loans issued against these deposits.

In active operations of banks, the main share is accounted for by credit operations and securities transactions. By issuing loans to their clients, commercial banks increase the money supply, and conversely, the repayment of these loans reduces the money supply in circulation.

One of the most complex and mystical aspects of money and credit is associated with lending operations. This is the so-called "multiple expansion of the money supply." To understand the essence of this phenomenon, we should introduce a new concept of “required bank reserves” - this is part of bank assets stored either in the form of cash in special bank safes, or (most of them) in the form of deposits in the accounts of the central bank. Reserves constitute only a certain percentage of bank deposits, which is established by the central bank and is mandatory for all financial institutions. A commercial bank can issue new loans and create bank money only if it has free or excess reserves, i.e. reserves exceeding the minimum amount established by law. There are two steps in this process:

¾ the central bank decides to limit official reserves to certain limits;

¾ The banking system transforms excess reserves into more bank money.

The size of this increase is determined by the so-called “money supply multiplier,” which is calculated as the inverse of the reserve requirement rate. Thus, if the banking system receives a certain amount of excess reserves (for example, from new deposits), it can increase the money supply by an amount equal to the excess reserves times the money supply multiplier. But the process can also go in the opposite direction, when a shortage of reserves leads to the destruction of deposits and a reduction in the supply of bank money.

In addition to lending operations, another type of banking operation is banking services. They include currency transactions, payment turnover, trust operations (management of client property by proxy), placement and storage of securities.

Along with the above-mentioned traditional banking operations, banking services such as leasing and factoring have recently become widely used. Leasing is the acquisition by a bank of property, such as computer equipment, for rent to users. This is a new form of financing that provides a number of advantages to both the lessor and the lessee. Factoring is the transfer by a company of the management of its receivables to the bank, which also undertakes the obligation to finance, as necessary, with the help of a loan, the fulfillment of all financial obligations of this company. Factoring is a universal system of customer service, including accounting, information, advertising, sales, insurance, credit and legal. Thanks to factoring, the turnover of funds in settlements is significantly accelerated.

Since banks are purely commercial enterprises, their goal is to make a profit. Gross profit consists of income from accounting and lending operations, interest and dividends from investments in securities, commissions from intermediary operations, income from external transactions, profits from founding and stock exchange transactions. A bank's net profit is the difference between gross profit and all costs of banking operations. The bank profit rate is the ratio of net profit to the bank's equity capital.

The role of commercial banks in a market economy is not limited to those functions discussed above. Very often, when they want to clarify the role of banks in the economy, they say that they act as intermediaries in the supply and demand of capital, especially short-term ones. In this case, their role should be to provide firms with funds raised by deposits. In fact, the role of banks is better described by the expression "banking industry", since it is much more important than that of ordinary intermediaries. Their main activity is the issue of means of payment.

The task of banks is to issue money in three ways, which differ in the equivalents of new banknotes: these are requirements for the economy, for the state treasury and foreign currency:

¾ as for lending to the economy, banks provide means of payment in the form of short-, medium- and long-term loans;

¾ in the case when banks subscribe to government securities, they convert payment claims to the state treasury into means of payment;

¾ By purchasing foreign currency, banks thereby transform payment requirements abroad into means of payment for domestic circulation.

Basic banking operations:

In general, repeating, banking operations include:

- attracting funds from individuals and legal entities to deposits (on demand and for a certain period);

- placing raised funds on your own behalf and at your own expense;

- opening and maintaining bank accounts for individuals and legal entities;

- carrying out settlements on behalf of individuals and legal entities, including correspondent banks, on their bank accounts;

- collection of funds, bills, payment and settlement documents, cash services for individuals and legal entities;

- purchase and sale of foreign currency in cash and non-cash forms;

- attraction of deposits and placement of precious metals;

- issuance of bank guarantees;

- making money transfers on behalf of individuals without opening bank accounts (except for postal transfers).

In addition to the listed banking operations, a credit institution has the right to carry out the following transactions:

- issuance of guarantees for third parties providing for the fulfillment of obligations in monetary form;

- acquisition of the right to demand from third parties the fulfillment of obligations in monetary form;

- trust management of funds and other property under agreements with individuals and legal entities;

- carrying out transactions with precious metals and precious stones in accordance with the legislation of the Republic of Kazakhstan;

- leasing to individuals and legal entities special premises or safes located in them for storing documents and valuables;

- leasing operations;

- provision of consulting and information services.

A credit institution has the right to carry out other transactions in accordance with the legislation of Kazakhstan.

All banking operations and other transactions are carried out in tenge, and if there is an appropriate license from the National. Bank - and in foreign currency. The rules for carrying out banking operations, including the rules for their material and technical support, are established by the National Bank. Bank of the Republic of Kazakhstan in accordance with the laws.

A credit organization is prohibited from engaging in production, trade and insurance activities.

INTRODUCTION

1 CONCEPT, ESSENCE AND TYPES OF PASSIVE OPERATIONS OF A COMMERCIAL BANK

2 DEPOSIT OPERATIONS

2.1 Features of deposit operations

2.2 Features of the analysis of the structure of raised funds

CONCLUSION

LIST OF SOURCES USED

INTRODUCTION

The economic basis of a bank's operations is cash flow. In a market economy, all operations of a commercial bank can be divided into three main groups:

- passive operations (operations to attract funds to the bank and generate its resources);

- active operations (allocation of bank resources);

- active-passive (commission, intermediary operations performed by the bank on behalf of clients for a certain fee).

Passive operations of commercial banks consist, first of all, in the formation of equity capital, which provides the first working capital. But the strength of the bank does not lie in its own capital. No matter how significant its own capital may be, the bank cannot be satisfied with it; in this case, its activities would be narrowly limited and such an enterprise would not be a bank. Actually, the functions of a banker begin from the moment when he utilizes other people's money, while he operates with his own funds, he is only a capitalist.

As a result of passive operations, commercial banks receive the necessary funds to finance active operations. The final results of these operations are reflected in the liability side of the bank’s balance sheet, where they act as sources of formation of its resources.

The object of this course work is banking operations.

Subject - passive operations: their meaning and implementation.

The purpose of this work is to clarify the concept, essence and main elements of passive operations of commercial banks.

1. Study the concept and essence of passive operations.

2. Consider the classification of commercial banks.

3. Find out the essence of deposit operations.

1 CONCEPT, ESSENCE AND TYPES OF PASSIVE OPERATIONS OF A COMMERCIAL BANK

1.1 The concept and essence of passive operations of commercial banks

Passive operations of commercial banks are operations to generate sources of funds and bank resources, which are reflected in the liability side of its balance sheet.

Commercial bank resources consist of two main types of sources:

- the bank's own funds and equivalent funds;

- raised funds.

It should be noted that a feature of the banking business is the fact that a commercial bank operates primarily on borrowed funds, which account for up to 90% of the bank’s total liabilities, while its own funds account for only 10%.

However, the analysis of a bank's liabilities usually begins with its own capital. Firstly, because without it it is hardly possible to start banking activities at all. Secondly, because the importance of equity capital in the bank’s activities is much more significant than its share in the total volume of liabilities. The bank's own capital is both its core of activity and the last reserve in case of unfavorable circumstances.

The role of equity capital and its importance for monitoring the activities of banks necessitated the determination of some indicator, using which it would be possible to recognize the amount of equity capital of a bank as evidence of its reliability, and the criterion of reliability would be recognized internationally. The difficulty in finding such an indicator was that it must be defined as a relative value, using which it would be possible to determine the capital adequacy under the operating conditions of a particular bank, taking into account the nature and structure of the services it provides.

The fact that the capital adequacy of a bank determines public confidence, both in a specific commercial bank and in the banking system as a whole, puts this indicator among the indicators under the constant control of the central bank.

Maintaining a sufficient level of capital is one of the conditions for the stability of the banking system. However, it is difficult and practically impossible to accurately determine the amount of equity capital that a bank or the banking system as a whole should have.

In the process of operation, the bank's authorized capital can and should increase. This is achieved by additional issue of shares and their distribution among legal entities and individuals through closed subscription or open sale.

In addition to the authorized one, commercial banks also have other own funds. These include the following:

- A reserve fund that serves to cover possible losses of the bank. Its size is determined by the bank’s Charter and is usually 15% of the authorized capital. The source of this fund, like all other bank funds, is profit.

- The Industrial and Social Development Fund serves to finance technical improvements in banking.

- The material incentive fund serves to encourage bank staff.

- The Fund of the Chairman of the Board of the Bank serves to finance areas not provided for by other funds of the bank.

In addition to the above, when banks improve large operations, banks create special insurance funds for the depreciation of investments in securities and possible losses on bank loans.

The bank's borrowed funds constitute the overwhelming majority of the commercial bank's resources. Carrying out passive operations allows the bank to attract temporarily free financial resources of legal entities and individuals.

1.2 Classification of passive operations of a commercial bank

The following groups can be distinguished as part of the passive operations of commercial banks:

- Deposits of legal entities and individuals;

- Balances on settlement, current and other similar accounts of legal entities;

- Loans from other commercial banks or the Central Bank of Russia (interbank loans);

- Issue of non-investment securities (certificates of deposit, bills, etc.)

A deposit is funds transferred to the bank for storage, subject to return upon maturity and certain conditions. The deposit amount is subject to return with payment of the interest rate established in the deposit agreement.

The types of deposit accounts used in the practice of modern banks are very diverse. In most countries, the classification of deposit accounts is based on two points:

The period of deposit until withdrawal;

According to the deadlines, they are distinguished:

- Deposits “on demand”, i.e. deposits repaid at the request of the depositor without prior notice;

- Time deposits.

Of course, term deposits are preferable for the bank, since the time of use of the funds is known, therefore the interest paid by the bank on time deposits is higher than on demand deposits.

- Accounts of individuals;

- Legal entity accounts;

- Government Accounts;

- Local Government Accounts;

- Foreign depositor accounts.

Demand deposits can be withdrawn from depositors or transferred to another person at the first request of the owner. In industrialized countries, demand deposits are withdrawn primarily by check, which is why they are called check deposits. The overwhelming majority of monetary transactions are carried out using demand deposits, which serve as means of circulation.

Currently, there are two types of demand deposits:

Interest-free;

Accounts that pay interest.

The former predominate in the total amount of demand deposits, while the latter are check deposits, which pay insignificant interest income.

Time deposits are credited to deposit accounts for a specified period and interest is paid on them. The bank enters into a written agreement with the deposit owners, which specifies the deposit amount, interest rate, deposit term, repayment date and other terms of the agreement. Before the payment is due, the depositor can withdraw the deposit only after prior notice to the bank, but in this case, as a rule, he loses interest income in the form of a penalty for early withdrawal of the deposit.

Since 1991, Russian banking practice began to use a type of time bank deposit, a time bank deposit, issued by a certificate of deposit. A certificate of deposit is a written certificate from the issuing bank about the deposit of funds, certifying the right of the depositor or his successor to receive, upon expiration of the established period, the amount of the deposit and interest on it.

Deposits are the main source of banking resources. The structure of deposits in commercial banks changes depending on the conditions of the money market and state regulation of interest rates on deposits.

Carrying out passive operations related to deposits, bank managers control the situation, taking into account the volume of costs for different categories of deposits, possible risks, and make efforts to grow the attracted deposits and optimize their structure.

It is necessary, however, to keep in mind that the peculiarity of this group of liabilities is that the bank has little control over the volume of such operations, since the initiative to invest funds certainly comes from the depositors themselves.

At the same time, as practice shows, all the efforts of bank managers are often ineffective, since the motivation for the behavior of depositors can be quite unique and difficult to predict.

Other sources of banking resources are funds that the bank independently attracts in order to ensure its liquidity. These may be interbank loans; securities sold under repurchase agreements; loans on the Eurodollar market. These are called managed liabilities. These liabilities give banks the opportunity to make up for deposit losses and be prepared for unforeseen circumstances.

Interbank transactions generally show the degree of development of correspondent relations between banks. Banks can receive loans from other banks, which gives them the opportunity to operate fairly large funds, maintain an optimal balance in the correspondent account and, if necessary, apply for a loan from a correspondent bank.

Obtaining a loan from the Central Bank of the Russian Federation is a traditional passive operation of commercial banks. Commercial banks receive loans from the Central Bank of the Russian Federation in the form of rediscounting and re-pledge of bills, in the order of refinancing, as well as in the form of a pawn loan, i.e. secured by government securities.

Repurchase agreements (repo transactions) emerged as new sources of resources for commercial banks. Such an agreement can be concluded between the bank and the company. If a firm wants to invest a large amount of cash for a very short period, it invests it in a repurchase agreement. The bank transfers securities to the company with obligations to buy them back after a certain period at a higher price. The difference between these prices is the actual fee for the loan provided to the bank.

Since 1993, operations to raise funds by issuing bank bills have become widespread. A bill of exchange is convenient because, unlike a deposit or savings certificate, it can be used as a means of payment. In addition, bills of exchange are not subject to registration, like other securities, which makes it easier for banks to work with them and makes it possible for them to be widely used, although the N-13 standard regulates their issuance by commercial banks.

The bank issues two types of bills:

- Interest;

- Discount.

The peculiarity of an interest-bearing bill is that the issue and sale of bills to legal entities and individuals is carried out at par value, with the subsequent accrual of interest on the bill amount.

The peculiarity of a discount bill is that it is issued and sold at a price below par, and repaid at par. The difference between the redemption price and the purchase price is the income of the note holder.

Eurocurrency loans are a financial instrument for managing passive operations, operating on the basis of deposits denominated in foreign currency and kept in commercial banks of a given country.

2 DEPOSIT OPERATIONS

2.1 Features of deposit operations

Deposit operations are one of the main banking operations. Acceptance of deposits, that is, deposits, is a loan transaction entered into by a bank from a person who owns capital for which it does not temporarily need, or for which the owner himself cannot find a use. By accepting deposits from the population, banks generate working capital, with the help of which investments are made in the national economy.

The word “deposit” comes from the Latin word “depositum”, that is, “delivery for storage.” Initially, due to the unsafety of storing savings at home, the public gave their money to banks for safekeeping, paying them certain interest for this service. At the same time, clients retained ownership of the amounts they contributed and could receive them at any time. Banks had the right to dispose of deposits accepted for storage. However, banks soon came to the conclusion that, despite more or less strong trust in them, the number of deposits still does not increase, despite their constant change. Therefore, banks decided to use deposits for their operations. At first, this was done secretly, since banks did not legally have the right to distribute the property entrusted to them for safekeeping. But when practice proved the complete safety of such operations, the banks began to act openly. They began to attract money to use in their turnover, paying depositors a certain percentage for this. Deposits for storage gradually turned into deposits for use. Therefore, banks, instead of collecting fees from depositors for storing amounts, began to pay them interest for use, which led to a fundamental change in the legal nature of the deposit.

Commercial banks provide an extremely important service for all sectors of the economy, ensuring the accumulation of savings and their subsequent use for various economic and social needs. On savings placed in the bank, which are completely safe and highly qualified, the depositor receives interest in the form of interest. Concentrated savings can be borrowed by entrepreneurs to expand production capacity and by consumers to purchase homes and consumer goods. A large share of this money is concentrated in the savings departments of commercial banks.

From the legal side, a deposit is a money loan agreement in which the borrower is a bank; lender - depositor. There is an opinion in Western literature that, based on the historical origin of modern bank deposits and in accordance with the commercial side of the matter, tends to give a different legal qualification to demand deposits. Proponents of the opinion proceed from the indisputable fact that modern deposits arose on the basis of a deposit (storage) agreement with bankers of the money that they then put into circulation. In addition, a deposit, as opposed to a loan, does not arise because a person in need of money, as usually happens, looks for a lender, but, on the contrary: in this case, the initiative belongs to the creditor, who himself offers money to the debtor. These circumstances prompt us to see in a bank deposit a special type of deposit agreement, that is, an irregular deposit - depositum irregulare - an institution known to Roman law and which has retained its importance in the modern world when depositing impersonal securities.

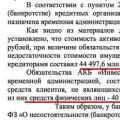

Commercial banks widely attract borrowed funds, through which almost 93% of total assets are formed. Thanks to the use of fairly cheap borrowed funds, including deposits, the relatively small profits from banking operations ultimately reach levels that provide shareholders with an acceptable return. The main source of funds raised is deposits, accounting for almost 86% of all liabilities of commercial banks.

The ability to post certificates of deposit and borrow Eurodollars or Federal Reserve Funds allows the bank to be less dependent on low-yielding secondary reserve assets, increasing its ability to make a profit. However, these operations come with risks. In managing passive operations, it is necessary to take into account this additional risk and, in addition, the relationship between the costs of raising funds and the income that can be obtained from investing these funds in loans or securities. Therefore, the relationship between asset management and liability management is critical to a bank's profitability. The operation of preserving values, that is, depot, has two forms: closed and open. The latter is divided into a depot for storing valuables and a depot for managing them. In a closed deposit, the bank accepts for storage valuables sealed in an envelope, for example, when the object of the deposit is securities or any documents, and in a box, when such objects are gold or other valuables. The bank charges a small fee for storage. For closed deposits, banks often use a system of renting out fireproof boxes (safes). Valuables are placed in these boxes and locked with two different keys, one of which is given to the client, and the other remains in the bank. In addition, an open deposit involves not only the delivery of valuables unsealed by the bank for storage (in the case of securities), but the ability to manage them.

Next comes the second category of capital, the disposal of which is more limited to its owners. They are free only for a certain, predetermined time. Typically, these are the savings of individuals who have not yet decided how to use their savings. Merchants whose turnover does not require the use of all capital deliver to the bank amounts that they have had for some time without use. Such deposits are term deposits.

The third type of available funds is capital for which the owners cannot accurately determine when they will need them. The owners are looking for premises that are profitable for them. Therefore, such funds must remain mobile, and their owners must have the right to withdraw them at any time. Such capital remains in banks for a short time and is called perpetual. According to Z.P. Evzlin and V.A. Dmitriev-Mamonov, “this category of deposits... is falling, since capital for which they want to receive interest is more profitable to place as time deposits, and capital for which they want to maintain mobility is more convenient ...deposit into a current account.”

Thus, depending on the length of time during which deposits remain at the disposal of banks, they should be divided into: long-term or permanent; urgent; unlimited or on demand.

The difference between these types of deposits, however, is not limited to the difference in the timing or procedure for placing and receiving them back. First of all, the amount of interest on time deposits, unlike permanent deposits or deposits to a current account, is predetermined, while on the latter type of deposits the interest paid by the bank is not determined in advance, but corresponds to the amount of the total interest established by the bank when accepting the deposit. In connection with the reduction of this amount, the amount of interest paid on this deposit may also be reduced. Finally, the difference between these types of deposits is that for the first two types of deposits (fixed and perpetual), deposit notes are issued, which are debt documents that serve as unconditional proof not only of the availability of debt savings, but also the amount of the debt itself. For current accounts, a payment book is issued, the entry in which only indicates the existence of a current account and the amount of the contribution made on a given day, but nothing is said about the actual amount of debt on a given date.

However, it is clear that many different kinds of depositors—individuals, business firms, non-profit organizations, government agencies, and local governments—will willingly place funds in commercial banks.

Demand deposits can be withdrawn by the depositor without prior notice to the bank. Such deposits are made by those who require funds in liquid form, and they account for 38% of all bank deposits. Demand deposits withdrawn by check account for almost 74% of the money supply. The reasons for the popularity of checks are obvious. This is an economical and safe method of transferring significant amounts from the point of view of transport costs and possible losses from robberies. When using checks, transfers are made by mutually offsetting claims between banks, and this does not cause much trouble for either the payer or the recipient. The check drawer is not at all worried about the possibility of forgery, since when paying a counterfeit check, the blame falls on the bank. Check circulation also has the advantage that the paid check is returned to the account owner and serves as a receipt for payment.

The check for a currency note, based on bank deposits, occupied a large place in the field of circulation and received a lot of attention in the economic literature. As Z.S. Katsenelenbaum notes, “a check represents an order issued to the banker from whom the person has a deposit to pay the bearer the amount of money indicated in the order.” The check is usually written on a special form received by the depositor from the bank. A check issued by a depositor and given to another person for payment for goods or repayment of any obligation takes on the character of money. The check is based on the cash deposit in a bank. In this sense, the check sets the “bank money” in motion.

To ensure settlements and payments, the bank opens current accounts and issues check books.

Historically, a check, like a banknote, evolved from a deposit. By transferring a certain amount to a banker for safekeeping in the form of deposits, the depositor himself could condition his right to receive back the deposited amount in two ways: he could agree with the banker that the latter would give him the entire amount upon presentation of his banker’s receipt, or he could agree that the banker will pay this amount in full or in parts, as required by the depositor.

According to the method of calculation, a distinction is made between settlement and transfer (offset) checks. The first ones are intended for the payment of cash amounts on them, and the second ones are only for transferring money amounts from one account to another, for offsetting them against the mutual obligations of various persons. Checks of the second category come in various forms, depending on whether the check is presented to the bank by the depositor whose account is credited or by the depositor whose account is debited. In the first case, we are dealing with an ordinary check, in the second - with a transferable check in the proper sense of the word, since this check cannot have any other purpose other than transferring an amount from an account to an account.

It is customary to distinguish between active and passive check legal capacity. Active checking capacity is the power to issue checks. Such legal capacity, as well as the ability to acquire checks and transfer them further, belongs to all persons with general civil legal capacity. In the case of passive legal capacity, only the bank can be the payer of the check.

Another type of time deposits are time certificates of deposit, which are a monetary document certifying the deposit of funds into the bank for a certain time and can be transferred or not transferred to other owners by endorsement. These deposits can only be withdrawn upon presentation of a properly endorsed certificate. They are recorded in the bank's general ledger under the heading "Time Certificates of Deposit", rather than in individual books under the name of the person to whom the certificate is issued, as is the practice with regular savings accounts. There are several types of certificates of deposit. Thus, many large banks issue transferable certificates of deposit to large holders. Banks are also seeking to attract smaller investors through short-term money market certificates. And a deposit known as a savings certificate is similar to a certificate of deposit in that it is issued for a specified period, usually three years.

Banks attract the cash reserves of entrepreneurs in their area, pledging to make the necessary payments at their request. The bank becomes the cashier of a whole group of enterprises that give their temporarily free money to the bank. An entrepreneur, having transferred his cash register to the bank, treats the bank cash desk as his own. The bank opens an account for him, which is in continuous movement, increasing with each new contribution, or falling with each borrowing made by the depositor from the funds entrusted to the bank. For this reason, these accounts are called current (conto corrento, somptes couserants).

By establishing current accounts in a bank, the cash registers of a number of enterprises located in the same area are united. The bank, as the cashier of its clients, is obligated to fulfill various commission payments of its clients. The interest they receive from the use of such amounts must then stand in a certain proportion to the amount of “trouble” involved in maintaining the clients’ accounts.

There is also a special demand current account secured by goods and valuables or an on call account, which means that a loan is opened to the client secured by goods or other valuables, in particular securities, foreign currency or bills, and the client has the right to receive the amount of the loan opened to him in installments and repay in installments. Both parties can liquidate their relationship at any time: the bank by closing the loan and demanding repayment of the debt, and the client by paying the amount of his debt and claiming collateral. In addition, to carry out this operation, an account similar to a simple current account is opened for the client in the bank’s books, which is why this account is called a special (active) account.

In recent years, banks have begun to face serious competition in the area of attracting savings and time deposits. Commercial banks compete across the entire range of investment activities, with the most intense competition coming from thrifts and savings associations, mutual savings banks, and credit unions.

For banks, maintaining savings accounts with a book is associated with additional costs: processing transactions is labor-intensive, it is necessary to maintain double records - in the account and in the book, conflicts often arise due to discrepancies in records, books are lost or stolen, etc. Some banks are trying to replace the books with a monthly account statement generated by the bank's computer and sent to the account holder. At the same time, the bank offers the client additional benefits: higher interest rates, bonuses, etc. In most cases, however, passbook holders do not want a replacement, and this labor-intensive type of service is still practiced by most banks. In an environment of intense competition for savings, banking practice has come up in recent years with some new types of deposits that provide customers with additional convenience and increase the liquidity of deposited funds. An example of this is the so-called ATC accounts; thus, there are savings accounts from which the bank automatically transfers money to the client’s current account if an overdraft occurs there.

The rapid growth of deposits was largely predetermined by the entry into force of the compulsory deposit insurance system. This factor played a decisive role in restoring depositors' confidence in banks. At the end of December 2005, the Federal Law “On Insurance of Individuals’ Deposits in Banks of the Russian Federation” came into force. To date, 932 banks have already joined the deposit insurance system (DIS), having passed the Central Bank’s selection process—almost all those who wanted to do so. The volume of funds in the Deposit Insurance Fund exceeded 20 billion rubles, and twice since its founding the Deposit Insurance Agency (DIA) has already had to pay citizens the money guaranteed to them by law - this is the interim result of the system’s work. In addition, the CER played an important role in the post-crisis restoration of confidence in the Russian bank.

If we summarize the advantages acquired by the banking system from the introduction of a system of state guarantees, we can distinguish three macro-effects. The first is an increase in the scale of the influx of money into commercial banks. Last year, Russian banks increased the volume of funds attracted for deposits in rubles and foreign currencies by 44.2% - up to 3825.5 billion rubles. Almost three quarters of them - 2,754.6 billion rubles (that is, almost $100 billion) - were received by banks that were included in the DIS. “In 2004 there was a failure, a slowdown in growth rates, but now deposits have again reached the growth rates that were in the pre-problem period.

The second macro-effect of the introduction of CERs is a sharp intensification of competition and the struggle for depositors between large and medium-sized banks with a significant strengthening of the positions of the latter.

Another trend is the reduction of Sberbank’s market share and the end of the short-term trend that arose after the problematic situation in 2004, when Sberbank won back a significant part of its clientele. Today this advantage has disappeared, and over the past year the share of private deposits in Sberbank has decreased from 60 to 54%.

2.2 Features of the analysis of the structure of raised funds

To analyze the structure of raised funds, comparative qualitative analysis and quantitative analysis are used.

A comparative qualitative analysis of the structure of raised funds is carried out by clients and terms, which makes it possible to identify from which sectors of the economy and for what period funds are attracted to the bank.

Quantitative analysis of the structure of raised funds consists of determining the share of each subgroup. Such an analysis gives us the opportunity to identify the role of each economic contract in the development of the bank's passive operations.

Using methods of comparative analysis of passive transactions, we identify changes in the volumes of these transactions and determine their impact on the bank’s liquidity.

To analyze the resource base, the amount of funds raised is calculated as of the beginning of each quarter, and in addition, at the end of the year.

The data obtained allow us to assess the dynamics of attracted funds from a commercial bank and draw the necessary conclusions: either a commercial bank is pursuing an aggressive policy and trying to sharply increase the volume of its operations, or it is adhering to a policy of moderate growth.

Analysis of the structure of attracted funds allows us to assess the significance of each source for the bank and their dynamics, thus determining the bank’s exposure to various types of banking risks. If interbank loans predominate among the funds raised, then in conditions of inflation the bank becomes dangerously dependent on the market situation.

Current funds are not only the most monetary, but also the most unpredictable instrument, therefore their high role weakens the bank's liquidity and thereby does not allow the bank to conduct highly profitable operations.

Foreign practice in assessing the stability of liabilities classifies the following resources as stable sources:

- Balances on settlement and current accounts;

- Demand accounts;

- Savings accounts;

- Time deposits of small denomination;

- Certificates of deposit up to $100 thousand (limit of insurance liability).

Non-permanent (unstable) resources include:

- Brokerage deposits;

- Certificates of deposit over 100 thousand dollars;

- Money market deposits.

The modern structure of the resource base of commercial banks, as a rule, is characterized by a small share of their own funds. In countries with developed market relations, the share of own funds in the composition of resources is determined by 15-20%, which makes it possible to ensure sufficient stability of banks and their sustainability. Own capital in the composition of the resources of Russian banks is no more than 10%.

The bulk of banks' resources are formed by borrowed funds, which cover from 80 to 90% of the total need for funds to carry out active banking operations. The maximum amount of funds raised depends on the bank's own capital. In different countries there are different standards for the ratio between equity capital and borrowed funds. These standards range from a ratio of 1:10 to 1:100. For example, in Switzerland this ratio is 1:12, and in Japan it is 1:83.

CONCLUSION

So, by passive we mean such operations of banks, as a result of which there is an increase in funds held in passive accounts or active-passive accounts in terms of the excess of liabilities over assets.

Passive operations play an important role for commercial banks. It is with their help that banks acquire credit resources in the money markets.

There are 4 forms of passive operations of commercial banks:

- primary issue of securities;

- deductions from bank profits for the formation or increase of funds;

- loans and borrowings received from other legal entities

- deposit operations.

Passive operations allow banks to attract funds already in circulation. New resources are created by the banking system as a result of active credit operations. With the help of the first two forms of passive operations, the first large group of credit resources is created - own resources. The following two forms of passive operations create the second large group of resources - borrowed, or attracted, credit resources. The bank's own resources are bank capital and items equivalent to it. The role and amount of equity capital of commercial banks are particularly specific, differing from enterprises and organizations engaged in other types of activities in that banks cover less than 10% of the total need for funds with their own capital. Typically, the state sets for banks a minimum ratio between their own and borrowed resources.

The importance of the bank's own resources is, first of all, to maintain its stability. At the initial stage of creating a bank, it is the own funds that cover the primary expenses, without which the bank cannot begin its activities. Using their own resources, banks create the reserves they need. Finally, own resources are the main source of investment in long-term assets. The structure of share capital of different banks is heterogeneous.

LIST OF SOURCES USED

- Banking / Edited by V.I. Kolesnikova, L.P. Krolivetskoy M., Finance and Statistics. - 2005. - 231 p.

- Beloglazova G.N. Money, credit, banks: A manual for universities. M.: Yurayt-Izdat, 2006. - 158 p.

- Joseph F. Sinkey. Financial management in commercial banks / trans. from English - M., 2004. - 733 p.

- Zhukov E.F., Maksimova L.M. Banks and banking operations. M., Finance and Statistics, 2005. - 342 p.

- Kozlov A.I. Money, credit, banks: lecture notes. - N.Novgorod: NIMB, 2003. - 278 p.

- Lavrushin O.I., Mamonova I.D. Banking. M., Banks and exchanges. - 2000. - 334 p.

- Sviridov O.Yu. Money, credit, banks: Textbook. - M: ICC "MarT", 2004. - 480 p.

Passive operations of a commercial bank are the activities of the bank to accumulate its own and borrowed funds for the purpose of their placement.

The purpose of commercial bank operations is as follows:

providing resources for the bank's activities;

formation of additional sources of funds for productive use in the economy;

increasing the income of individuals and legal entities receiving bank interest on deposits;

growth of the bank's equity capital;

creation of reserve funds for insurance of banking operations.

Passive Operations- operations to mobilize funds, namely: attracting loans, deposits (deposits, savings), obtaining loans from other banks, issuing own securities. Funds received as a result of passive operations are the basis of direct banking activities. Active operations - operations for placing funds. As a result of active operations, banks receive debit interest, which should be higher than the credit interest paid by the bank on passive operations. profit is also generated from commission fees for banking services).

Basic Passive Operations commercial bank - deposit.

Deposit operations- These are fixed-term and permanent investments of bank clients. Funds held in demand accounts (demand deposits) are intended for making current payments - in cash or through a bank using checks, credit cards or letters of credit. Another type of deposits is time deposits (with certain maturities). These deposits usually pay higher interest depending on the term of the deposit, since banks can manage the depositor's funds for a longer period of time and have the opportunity to reinvest them.

Passive transactions also include various savings transactions. Savings deposits serve to accumulate client funds, of which the client is issued a certificate (savings book). Passive operations of a commercial bank include:

creation and increase of equity capital through deductions from profits;

issue of securities and their placement on the open market;

deposit operations;

interbank loans on the domestic and foreign markets (Fig. 74).

Among deposit operations The following groups are distinguished:

demand deposits;

time and savings deposits.

Active operations of banks - these are operations for issuing (placing) various types of loans. The most common type of credit issued by banks is a short-term loan to economic agents, usually to finance the purchase of inventories. This loan may be issued with or without actual collateral, but in any case, in order to obtain it, it is necessary to have reported financial documents characterizing the financial position of the borrower so that the bank can at any time assess the likelihood of timely repayment of the loan.

16 Management structure of a commercial bank

The organizational structure of a commercial bank can be viewed from two points of view. On the one hand, it is a system of transmitting orders from higher authorities to lower ones. On the other hand, it acts as a system of division of powers between authorities. It determines the internal conflict potential of the bank associated with possible intersections of the areas of competence of various management subjects. The speed of information flow and the level of conflict potential depend primarily on what organizational management structure will be chosen.

In order for the connections between the elements, which are units and employees, to be not random, but orderly and purposeful, the relationship of dependence or subordination between the object and the subject of the organizational structure must be regulated, which is established by the distribution of functions (division of labor).

It follows from this that the effectiveness of any process - its reliability, efficiency, productivity - directly depends on the quality and adequacy of the bank’s organizational structure to external and internal changes, i.e. from the distribution of responsibility for the performance of bank functions between departments and tasks between employees, authority to make strategic, tactical and operational decisions.

Now let's look at the classification of organizational structures of commercial banks. There are two main classes of organizational structures: mechanistic and organic. Despite the fact that this division is well-established and generally accepted, there are also other names for the named classes. For example, bureaucratic and adaptive structures. In this work, we will use the definitions “mechanistic” and “organic” to name classes of organizational structures.

The management structure of a bank includes functional divisions and services, the number of which is determined by the economic content and volume of operations performed by the bank, which are reflected in the License for the bank to carry out banking activities. Typically, the management structure of a commercial bank includes the following divisions and services:

management of deposit and deposit operations;

management of cash transactions;

customer service management;

accounting and reporting department;

internal control department;

currency management;

legal management;

credit management;

investment management;

Bank Securities and Financial Services Department;

Marketing Department;

management of work with the bank's branch network;

department of security and internal security of the bank;

administrative and economic management;

economic planning management.