Vladimir Malakhov, General Director of Modern Technologies of General Contract Management LLC, Ph.D. Sc., Doctor of Business Administration:

– A logical and expected consequence of the increased discussion about engineering was the emergence of an active dialogue about the role and place of engineering companies in the country’s economy. Discussion of engineering issues, initiated by instructions from D.A. Medvedev dated May 23, 2013 on the creation of a “Road Map” (Action Plan) in the field of engineering and industrial design, reached a new stage after a number of programs and individual events appeared to support engineering companies of small and medium-sized businesses. Moreover, resolutions have appeared on the creation of regional engineering centers and centers of engineering competence, which, according to their initiators, should become centers of concentration for a new structure for the development of national engineering. Whether this is real or not, time will tell. However, a preliminary answer to this question was given by one of the leaders of the Ulyanovsk region: “Why do we still need additional bureaucratic structures in the field of engineering and support for SMEs, when there already exists a whole range of similar or similar in functionality programs, institutes and divisions, starting from cluster centers and industrial development of regions and ending with all kinds of support structures for local manufacturers and SMEs? There is no point in creating another stream of money from the federal budget that does not guarantee an obvious systemic result.” It is difficult to disagree, since the attitude and requirements towards so-called engineering companies cannot be formulated without a clear understanding. And you need to understand what it is.

ENGINEERING COMPANY STATUS

In order to draw certain conclusions about the status of an engineering company, it is necessary to first consider some of the controversial areas of this concept. Here are just the most controversial of them:

1. Comparison of engineering companies in terms of engineering classification. Among other classification bases, perhaps one of the most sensitive bases is the division according to the physical object of engineering (Engineering as the creation of useful, commercially usable information about the architecture of a physical object or the nature of a physical process). There are only two key types of physical objects: movable objects and real estate. This division suggests that we must assume completely different engineering companies. Companies designed to create new consumer goods, machines and mechanisms, machine tools and vehicles, tools and devices or other means of labor are more likely to be called not engineering, but engineering, design, architectural or even scientific and innovative.

When it comes to an engineering company, a critical mass of business representatives means a real estate development company. This is also the problem of correlating ideas of business turnover and consolidating legislative terminology. When we talk about supporting engineering companies, especially small and medium-sized businesses, we most likely mean companies that generate new means of labor, technologies and goods, and not real estate as a whole. That is why it is necessary to legally separate production engineering companies from companies engaged in investment and construction engineering.

2. Comparison of engineering and engineering companies. Another key contradiction in the understanding of engineering companies lies in its mental attachment to engineering and engineering in general. This conflict is aggravated by discrepancies in translation from foreign primary sources, when engineering is understood as engineering, design, and a set of specialized services to support investment and construction projects. Numerous experts most often quite rightly characterize the concept of engineering as a type of activity in the service sector, which is based on the concept of “engineer” or “engineering”. However, it is precisely this nuance that does not allow engineering companies and engineering business to be synonymous. First of all, from the point of view of the conceptual field and classification of engineering and engineering. Engineering includes a significant share non-technical engineering, i.e. services for transforming not only natural, but also other sciences into commercially useful information on the feasibility of creating physical objects and using physical processes. In other words, it contains a significant share of organizational, managerial and financial cost engineering. In the same time, engineering is limited to a natural science basis and does not set itself the task of creating commercially profitable results.

Moreover, engineering goes far beyond the so-called technical and technological engineering, since it is present both in research and development (R&D), and in experimental production and process modeling (R&D - Research & Development), which may not end with reaching the engineering stage of its life cycle. Thus, it must be stated in advance that only those business structures that are engaged in the reasonable transformation of the results of scientific research and research into market-demanded goods with added consumer value can be classified as engineering companies.

3. The role and place of engineering companies in the investment and construction sector in Russia and the world. Russian engineering companies engaged in investment and construction activities have long become the talk of the town among most customers of large investment and construction projects. Their main complaint comes down to the fact that many companies that call themselves engineering companies or even have such a word in their name, in fact, are not such. They do not meet customer requirements when providing engineering services! According to E4 Group OJSC, in Russia, about 7,000 companies nominate themselves as engineering companies in the investment and construction sector, of which no more than 200–500 actually have the right to consider themselves such. If we take into account global trends, the presence of at least one large engineering company in the national economy of a country is already considered a success. In addition, if you look at the top hundred engineering companies in the world, you will not find Russian companies there. From time to time, the Russian Stroytransgaz appears in the second hundred. However, these are more retrospective consequences of his past foreign activities than an objective assessment of the current level of engineering. The bulk of the world's largest engineering companies have annual revenues of at least 10 billion US dollars, and therefore we need to look for understandable and effective mechanisms for creating national engineering monsters.

The desire of experts to “bring the concept of an “engineering company” to a common denominator, even if it is limited exclusively to the investment and construction sphere, has become not just a reflection of professional interest in streamlining such activities, but also an objective economic task at the federal level. Creating conditions for the emergence, nurturing and preservation of our own engineering whales is impossible without government support. No country can afford to abandon a rare engineering business to the mercy of fate. In many national economies, gross income from engineering activities brings up to 20%. Russia also has a significant national interest in this and the same potential to achieve it. One gets the impression that while officially declaring their readiness to create and support engineering companies in the investment and construction sector of the economy, in fact there is a discussion of purely engineering issues, ranging from clarifying certification requirements for professional consulting engineers to bringing engineering activities under existing OKVED articles in the field of design and surveys , collection of initial permitting documentation and land management works. There are a number of other types of activities that require special attention for the safety of work and the life of participants in the process, but they do not provide grounds for including engineering activities in a separate article of OKVED.

MAIN AREAS OF WORK FOR FORMING A POOL OF ENGINEERING COMPANIES

Let's consider the main directions of work to form a pool of engineering companies in the investment and construction sector in Russia, depending on the problematic sources identified above.

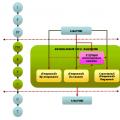

The situation with the creation of an institute of consulting engineers in Russia, by analogy with Western associations, requires proper registration. According to the Town Planning Code, the functions of a technical customer can also be performed by an individual. The question is the set of licenses that he must own to fulfill his obligations. A much more difficult question about the differences engineering And engineering companies in the investment and construction sector. Many experts consider them synonymous, but as a result, several thousand engineering or engineering companies nominate themselves as such, depending on their market mindset. I advocate a clear division of functionality and powers, confirmed by relevant documents.

The distinction between engineering companies and engineering companies should be based on similar considerations. For example, everyone understands perfectly well what a law office, clinic or shopping center is in the form of renting space for boutiques. This is a certain amount of licenses that allows each of their personal owners to carry out personal professional activities without restrictions. Income from personal activities is key, and income from temporary pooling of licenses to create integrated services is periodic and optional. This is how an engineering company should work, which is an algebraic collection of licenses of consulting engineers who can temporarily unite to implement a common project and obtain the necessary corporate certificates for this. However, this association is not liable after its dissolution. Everyone remains responsible within the limits of their personal license.

The engineering company not only provides integral products, but also bears responsibility for the product after it is put into operation. She is responsible for corporate decisions with all her property, and sometimes with the property of the founders. It gives guarantees no matter where and how many licensed specialists it has, since it must have a special document from an engineering company, for example, certified project management system, and knowledge management system certificate, allowing you to claim special compensation for engineering services. In addition, such a company must have its own fund of intangible assets, in the form of registered ownership rights to corporate intellectual products. The right to compensation for engineering services is a key prerogative of such a company. It is under these conditions that a small circle of large engineering companies and a wide range of engineering consulting businesses will be formed, as well as a significant number of independent consulting engineers. Conventionally, this hierarchy can be built like this:

THREE PITCHES OF AN ENGINEERING COMPANY

If we start from the specifics of an engineering company, we can almost immediately conclude that with such volumes of responsibility, there are very few really powerful and sustainable engineering companies. Such a company can be briefly characterized as follows: an engineering company in the investment and construction sector is a unique organizational and legal formalization of activities for the provision of comprehensive engineering and consulting services for the implementation of investment and construction projects, including real estate redevelopment projects. Even this definition does not allow literally every specialist in the investment and construction sector to be sure that he works in an engineering company. Most experts are inclined to the following set of mandatory attributes specific to an institutional engineering company in the investment and construction sector.

In addition to the mentioned features of engineering companies, experts cite up to 30 different factors that allow us to say that you work for an engineering company. This includes access to the financial market, the presence of a system of self-sufficient financing, a guaranteed life cycle of already contracted projects, and others. It is reasonable to dwell on key factors that can not only be standardized and described from the point of view of technical regulation, but also set up a system of certification and periodic audits.

THREE MAIN CRITERIA FOR AN ENGINEERING COMPANY

1. Certified knowledge management system. If engineering is the activity of providing services for transforming scientific knowledge and achievements into intellectual products, then the engineering company will be the one that has a set of initial scientific knowledge. In order for scientific knowledge and achievements to be transformed into useful intellectual goods, a company must have not only a set or body of knowledge, but also confirmed rights to them, if they are not its property. The main feature of an engineering company is the presence knowledge base, and also tied to it knowledge management systems, or knowledge management systems (KMS). A knowledge management system is a set of interacting and interdependent elements related to knowledge management (processes, databases, software, organizational structures, etc.), ensuring the achievement of set goals. Knowledge management is a combination of individual aspects of personnel management, innovation and communication management, as well as the use of new information technologies in the management of organizations. Knowledge management is always a fusion of various disciplines, diverse approaches and concepts.

2. A certified management system specifically for investment and construction projects. Thoughtless application of any project management standards significantly complicates the procedures for managing real estate projects or lengthens the preparatory work so much that the meaning of many standard project management procedures is lost. Therefore, universal principles of project management should be specified by companies to the specifics of their investment and construction projects and not require over-competent decisions where common sense does not require it.

3. Personal corporate bank of intellectual products. From software and databases to them, to pricing, personnel training systems and project management in general. At the same time, intangible assets must be properly patented, registered, and their ownership should not raise doubts among competitors.

These three pillars of an engineering company will allow them to be separated from simply engineering and consulting firms, even if they are conducting projects that are quite significant in terms of capital investments. The main thing is post-project responsibility, which remains with the engineering company regardless of the top manager, owner and his views on the future of this company.

ASSESSMENT OF THE COST OF ENGINEERING COMPANY SERVICES

Why is it so necessary to separate the engineering company from the engineering company? First of all, this concerns responsibility for the results of such services. If in an engineering company we can safely talk about the responsibility of each license holder, as well as the joint responsibility of a group of consulting engineers within the limits of their compensation fund, then the engineering company is aimed at providing services to a non-professional consumer. She is responsible for the result as a whole and is responsible not only for the quality of design solutions, but also for their relevance, cost-effectiveness and compliance with the best construction practices and safety requirements at the time of drawing up the technical specifications. Such responsibility is comparable to lifelong responsibility. Of course, it is impossible to cover such liability 100%, but insurance instruments specifically for large-scale engineering are created for this purpose. Engineering companies themselves can be such only if they are capital-intensive, resource-rich and financially liquid. That's why there won't be many of them.

Most engineer license services today already have both aggregated and detailed cost estimates. The cost of an engineering company's services can only be the sum of tariffs and approved estimates. Of course, an engineering company can also take on the services of a general contractor who takes risks, that is, be responsible with all its capital for the result of the work and hire lower-level co-contractors. But in this situation, such a company has no right to claim any compensation that is not reflected in the estimated prices. In other words, in order to earn more, such a company will have to do some of the work on its own. Accordingly, they will never be able to become super-large, because their own forces are a significant depreciation load. The cost of an engineering company's services should be based on the difference between its future costs and some fixed price, regardless of the estimated prices. It may significantly exceed the standard norms of estimated profitability, but this will be justified by the value of the brand and the level of responsibility of the engineering company. Provided that the obligation of engineering and engineering companies to pay fixed rates to lower-level co-contractors for work performed can be established by law, competitions between engineering companies can be held specifically for the cost of the engineering margin or markup to the fixed cost of lower-level subcontracting services.

On the other hand, the item in the estimates about the costs of the customer-developer may become optional, since the costs of the investor and developer for their own project management can be decided by them independently. If this is a budget project, then such costs are clearly included in the amount of the engineering margin and are not allocated as a separate line.

CERTIFICATION SYSTEM FOR MANAGING PROJECT DIRECTORS

The efficiency of the functioning of an engineering company in the investment and construction sector is ensured not only by three pillars, but also by the presence of qualified project directors. Today, you can count on one hand the projects that one manager started and he also finished them. Such specialists in each country should be considered as the most valuable personnel. Conditions must be created that allow engineering companies to clearly identify themselves as such due to the presence of several certified project directors on their staff. Moreover, such a company has the right to increase the cost of its services if the customer requires that the project be managed by a certified specialist. The right to certification should be held by specialists who either participated in a project from start to finish, or managed a project without certification, at the employer’s own risk, but successfully completed and commissioned the project. The grade system in this case should motivate project directors to bring the project to completion, that is, the more projects he has completed, the more expensive it is for the engineering company and the customer, respectively. This will create a layer of project directors - aces who will be responsible for the results of work in their own name. The efficiency of implementation of investment and construction projects will increase significantly.

1. To provide in the upcoming draft “Law on Engineering Activities” a key classification of engineering, dividing all engineering services into services in regarding real estate and for services in regarding consumer products both B2B and B2C. The reason for this fundamental difference is not only the difference in the structure of the life cycle of products and real estate, but also the financial and organizational specifics of the implementation of such services. If in the first case we are talking about relatively small capital investments, then in the case of real estate engineering (or, to be more precise, investment and construction engineering) we are talking about very significant budget and capital injections, responsibility for the result of which borders on national importance. This also applies to real estate objects such as ships and space satellites. The analogies here are completely adequate.

2. Remove the concept and phrase “technical customer” from the Town Planning Code of Russia. Replace it with the unambiguous term “consulting engineer”, which can be either an individual or a legal entity that provides management services for investment and construction projects.

3. To legislate the legal difference between the services of consulting engineers in terms of the volume of risk of an investment and construction project. If a consulting engineer takes on the risk of a turnkey project, he must have all the guarantees for the facility, that is, meet the requirements of the engineering company. Such a contract is automatically considered a general contracting EPSM contract. The auditor of the quality of services of such performers can only be the state technical supervision body or a specialized supervisor authorized by it for the type of work, by analogy with the state examination. The same bodies are required to conduct ongoing monitoring of projects of non-professional investor-customers. If the consulting engineer does not take on the risk of implementing the project, then such an agreement is a contract for consulting services and is paid at approved rates. This is the market for engineering companies. In addition, a consulting engineer can be an individual with a license from the Ministry of Construction, who alone provides services to the retail market for non-professional clients. He can also work with engineering companies on a contract basis.

4. Introduce significant changes to the legislation on public procurement, requiring the mandatory involvement of EPC or EPC contractors for projects of non-professional investor-developers. Develop and implement a two-stage system for estimating the cost of projects for non-professional customers, including government agencies, involving a competition of cost proposals taking into account the engineering margin at the stage of selecting an EPC/EPCM contractor and approval of the final cost after examination of the project. If after examination of the project the cost, taking into account the margin, has increased, then the contract price remains at the level of the original offer. If the cost has decreased, then the percentage of the engineering margin in relation to the final SSR approved by the examination is maintained.

5. Create a system of responsibility for investors, customers or developers for the results of their project management, which would motivate the main holders of capital construction services at large industrial enterprises, investment companies and financial-industrial groups, to attract EPC or EPC contractors, as cheaper alternatives. Then our engineering market will revive and become a strong international player.

These efforts will not only allow the cluster of Russian engineering companies to revive, but also take their rightful place in the international engineering market.

In the press service of the Industry Center for Capital Construction of Rosatom (OCCS), the organizers of RISF-2015 were the Ministry of Construction and Housing and Communal Services of the Russian Federation, the National Association of Housing Developers, the National Association of Builders, the National Association of Designers and Surveyors, the National Agency for Low-Rise and Cottage Construction, the Foundation assistance to the development of housing construction, Agency for Housing Mortgage Lending.

Opening the all-Russian meeting “Investment potential of the Russian construction complex: current state, risks, development prospects,” the Minister of Construction and Housing and Communal Services of the Russian Federation Mikhail Men noted that, despite the difficult situation in the construction industry in 2014, the positive dynamics of the industry’s development have remained. “In 2014, 81 million square meters were built. m. of housing. Compared to 2013, the growth was 15%. This is a very serious breakthrough in development. For the first time in the history of modern Russia, we exceeded the indicators of the Soviet period of the RSFSR: In 1987, 72.8 million sq.m. were built. housing,” Men emphasized. He noted that the leading indicators of construction growth rates were recorded in the Sverdlovsk region, Krasnodar region, St. Petersburg, Moscow, Moscow region and Bashkiria. The head of the Russian Ministry of Construction said that today the Russian government is taking serious measures to support the construction industry, primarily this concerns mortgage support, since every third apartment in the country is sold through the mortgage lending system. “Thus, the mortgage lending support program, under which 20 billion rubles will be allocated to subsidize the interest rate on mortgage loans - the rate will not exceed 13%. In today’s conditions, this is a good figure,” he emphasized.

Deputy Mayor of Moscow Marat Khusnullin, who spoke at the meeting, noted that, despite the challenges of the time, the Moscow construction complex is not going to deviate from its plans. Thus, the plan of the Targeted Investment Program (TIP), the budget of which is 1 billion rubles, is scheduled for three years and will not be adjusted. As support for investors, the Moscow government is considering subsidizing interest rates and ensuring the provision of utilities. According to Khusnullin, the city will do everything to create jobs that would bring taxes to the budget. “We have invited all contractors to speed up construction work if possible. For our part, we are doing everything possible so that they can complete the construction ahead of schedule,” emphasized the Deputy Mayor of Moscow.

Commenting on the results of the all-Russian meeting, Gennady Sakharov, Director for Capital Investments of the Rosatom State Corporation, Director of the Rosatom OCKS, emphasized that “The Russian Investment and Construction Forum has become a representative platform where experts in the construction industry discuss the most important problems in this area.” “Today it is important to understand how to move forward in the current conditions, avoiding losses for the construction industry; you need to understand the development strategy of the construction industry. The forum touched upon the most important issues that are close to the construction complex of the nuclear industry, in particular, we plan to analyze whether the experience of the Moscow government can be used in the nuclear industry in terms of facilitating conditions for contractors participating in tenders - for example, the abolition of the mandatory provision of bank guarantees.” , Sakharov emphasized.

As part of the forum's business program, dozens of round tables were also held. The greatest interest and inspiration was generated by the round table dedicated to the development of the procurement system for construction services, moderated by the vice-president of the National Association of Builders (NOSTROY) Eduard Dadov. There was a large-scale discussion about what the new law on procurement in construction should be like. The main report was made by the director of the International Institute for the Development of the Contract System, Pavel Kolykhalov, who stated that the draft law being developed will concern all entities involved in construction activities. The main innovation will be the obligation of the contractor to carry out at least 75% of the work on its own, as well as the introduction of a rule on the provision of a qualification certificate, which is expected to be issued by an SRO. The chairman of the Committee on Competition Policy and Procurement in the Construction Sphere of NOSTROYA, Valery Mozolevsky, spoke out against this norm. He emphasized that “responsibility for the construction and safety of the facility falls on the customer, and not on the SRO.” Vladimir Malakhov, Deputy Director of the Rosatom Center for Engineering, who spoke at the round table, noted that a new procurement law is necessary because procurement of construction services is fundamentally different from procurement of materials and any other goods. “I am convinced that it is necessary to legislatively change the situation with pricing in construction - the last price should be the price of a conditional worker with a trowel, that is, the price of the final contractor, and the general contractor should compete for the general contracting margin, which should not exceed 20%,” said Vladimir Malakhov .

The round table on the topic: “Development of the Institute of Technical Customers” was also very popular among the forum participants. Standard contracts in construction." Thus, the majority of the discussion participants were of the opinion that the institution of technical customer should be developed in close connection with the development of standard technical specifications, standard contracts and other documentation. “The technical customer service should be a team of experts who can competently perform any work at all stages of construction: from surveys and design to attracting financing for a specific project,” noted Natalya Rotmistrova, a representative of SRO NP MAAP. She emphasized that standard documentation is designed to make the work of a non-professional customer easier. Vladimir Malakhov, Deputy Director of OCKS for Engineering, who spoke at the round table, proposed replacing the term “technical customer” with the international term “consulting engineer”, widely used throughout the world. “I believe that the technical customer responsible for construction results is the general contractor. According to the Urban Planning Code, the technical customer has about 30 functions, and only 4 of them are strictly technical, related to obtaining licenses and permits for the construction of a facility. Everything else is pure consulting. It turns out that the technical customer is forced to do the work that consulting engineers and technical consultants do. This is their direct work,” said Vladimir Malakhov.

Later, there was a visit to the forum’s exhibition exposition, where a wide range of investment construction projects from all over the Russian Federation was presented. In total, 250 exhibitors were presented at the exhibition, including 41 investment projects that reached the finals of the first Urban Planning Competition of the Ministry of Construction and Housing and Communal Services of the Russian Federation. The Industry Center for Capital Construction (OCCS) of Rosatom participated in the joint stand of the Russian Union of Builders.

The term "design" means the development or design of objects of various kinds. Sometimes design refers to the description and modeling of an object. To some extent, the term “engineering” is similar. In a broad sense, engineering means the creation or operation of objects of various...(Management Theory)

Control systems engineering

Design of the company's management system architecture Descriptions and engineering (development) of management systems can have different details and coverage of stages of the full management cycle, for example: o analysis of the situation and clarification of management goals; o identification, documentation and regulation of the main...(Management Theory)

TERMINOLOGICAL APPARATUS, CONCEPTUAL AND METHODOLOGICAL FUNDAMENTALS OF LOGISTICS

Logistics concept The main areas of application of the concept of "logistics" The term "logistics", known until the beginning of this century only to a narrow circle of specialists, is now becoming widespread. The main reason for this phenomenon is that the concept began to be used...(Logistics)

Conceptual basis for developing management decisions

In the process of managing business entities, a huge number of very diverse decisions are made that have different characteristics. However, there are some common features that allow this set to be classified in a certain way. This classification is presented in table....(Enterprise economy)

Financial system and financial policy

Financial relations and the financial system A market economy presupposes the functioning of monetary relations. Their sphere is huge. They service commodity transactions and the relationships of enterprises with each other. In addition, all commercial and government organizations, as well as their employees, are involved...(Economic theory)

Financial relations and the financial system

A market economy presupposes the functioning of monetary relations. Their sphere is huge. They service commodity transactions and the relationships of enterprises with each other. In addition, all commercial and government organizations, as well as their employees, are drawn into a circle of monetary relations with the state and its institutions...(Economic theory)

As the civilized market of EPC/M-contractors is formed in Russia, the majority of participants in the investment and construction process (hereinafter referred to as ICP) are gradually coming to understand that the real market of EPC/M-contracts is far from the theoretical ideals of such an approach, and in some cases it completely contradicts basic settings of the EPC/M model. And the point is not so much that the majority of EPC/M-contractors are currently not ready to meet the entire set of requirements for the implementation of such projects, but rather that the majority of Customers have turned the EPC/M-contract into a way of maximizing risk relief even where the specifics of a particular COI do not imply this.

Of course, this also includes some of the inflated ambitions of the EPC contractors themselves, who today take on the entire range of risks and obligations of such a contract and sometimes beyond that, without giving due account of their capabilities and counting only on the probabilistic growth potential. This conclusion can be made based on an analysis of several dozen websites of construction companies declaring their readiness for EPC/M contracts, and if we add here those who are not actively presenting themselves, the conclusions become disappointing: EPC/M contracting has become a fashionable attribute construction business. At the same time, many Customers, as if following the administrative fashion of the energy industry’s investment program, unanimously rushed to formulate the terms of EPC/M contracts, without even bothering to analyze their necessity, relevance, relevance and economic feasibility.

Today, it is no secret to anyone that the EPC/M contracting market is in its infancy in Russia and it is unlikely that in the current market situation it is possible to find ideal models for the implementation of such contracts. Various hybrid models are in use, which are becoming more and more optimal in terms of risks and costs for Customers. As a rule, they largely combine the individual theoretical principles of the EPC and EPCM models. For example, an EPC/M contractor may not take on the risks of fluctuations in labor tariffs, but at the same time guarantee the quality of work and standard productivity in accordance with the construction and installation work schedule fixed in the contract. Taking into account the high dynamics of prices for materials, the increase in cost of which causes biased marginal coverage of the risks of fluctuations in the future, may be paid by the Customer at the actual cost or adjusted according to an algorithm previously agreed with the Customer. In general, the emergence of the EPC/M services market will lead to the emergence of new innovative schemes for implementing contractual strategies, which will ultimately lead to an increase in Customers' budgets due to higher reserves to cover risks and unforeseen circumstances.

Understanding the real processes taking place in the EPC/M contracts market is necessary for accurate segmental positioning of construction contract participants at the stages of the investment and construction process, which will subsequently become the basis for the formation of the competitive competencies of each company. To this end, within the framework of this article, various options for implementing EPC/M-approaches, their real semantic and economic content and the possibility of building an optimal structure for the interaction of all participants in the implementation of investment and construction projects using EPC/M-contracts will be considered and analyzed. At the same time, we will try to consider possible options for transforming contracts in the process of implementing the ISP in order to obtain maximum effect in all required indicators.

The activity of the Customer as a decisive factor in the applicability of EPC/EPCM contracts.

Today, many participants in the construction market do not take into account that historically the EPC/M contract appeared mainly due to budget financing of the construction of social facilities, thanks to charity and other forms of passive financing. Most often, such contracts were in demand where the exact amount of money allocated for a particular event was known, and the investor himself was not interested in the subsequent operation of the facility, much less in generating income. It is in this case that a conventional fixed-price turnkey contract (LSTK - Lump Sum Turn Key) reflects its true original meaning, namely, obtaining a product whose use is similar to buying a car at a known price - with the instant turn of a key. As when buying a car, the buyer remains a passive investor; he can choose the technical parameters of existing models, their design, contents, options, but he does not want to personally participate in their manufacture, assembly, project development and procurement of components. In this analogy, the EPC contract fully corresponds to purchasing a car directly from the automaker, subject to your financial constraints. While the EPSM contract is similar to buying a car from a car dealer, since you one way or another pay the seller a premium for managing the process of delivering the goods to the buyer, its sales service, and maybe support during production, if such were the terms of the contract.

In any case, the decisive factor in the formation of contractual relations using the EPC model was the passivity of the customer in relation to the construction project. This passivity could be due to both the natural status of the investor-customer and his vision of distributing risks and obtaining subsequent benefits from the implementation of the project. These considerations can be briefly characterized, for example, by the following limits of applicability of EPC models:

- Professional non-compliance of the Customer with the construction project;

- Limit of funds allocated for the purchase of a finished object;

- Lack of objective need to take responsibility for making technical decisions that are determined by other people’s requirements;

- Political, geographic, interstate, legal and other similar obstacles to active project management;

- The presence of ready-made market and technically proven solutions for ready-made objects within the framework of the EPC approach, which make it unnecessary to spend additional costs on searching for the best products.

And other reasons.

If the Customer takes an active position in the implementation of the contract, since this is due to his future decision to personally operate this facility or use it in any other way to make a profit in the future, the classic EPSM model becomes the most acceptable, but significantly transformed and brought to reality situation or the construction market in general, or a specific industry sector. This especially applies to almost all cases of implementation of projects for the construction of industrial facilities, the typical forms of EPCM contracting of which can be described as follows:

- Representative of a foreign Customer or investor. One of the most common options for implementing projects in which a foreign investor is interested. In this case, he enters into an agreement with the same foreign EPSM contractor, most often a stable partner of the Customer in foreign markets, who assumes the risks of financial control, construction quality and development of a design solution, but transfers as much as possible all country risks to local lower-level contractors and quite officially frees itself (with the knowledge of the customer, of course) from the risk of achieving production capacity and contract deadlines. Typically, a foreign EPSM contractor undertakes the development of a basic design and hires a Russian designer to adapt it and obtain working documentation, along with the entire package of initial permitting documentation, which certainly entails a whole range of problems. In order to maximize risk transfer, such a contract is usually aggravated by excessive warranty requirements and withholdings from Russian performers. Such a contractor can be schematically represented in Fig. 1.

Rice. 1. Foreign EPCM contractor with limited risks.

- The Customer's subsidiary is another common option for EPSM contracting. In Russia, the services of their 100% subsidiaries EPSM contractors are used by the majority of the largest institutional customers in the fuel and energy complex, ferrous and non-ferrous metallurgy, transport construction and other industries. There are completely objective explanations for the emergence of such EPC contractors, since Customers with a repeating set of objects and works, moreover, often connected into a single industrial complex, such as transport systems, pipelines and networks, do not need to constantly appeal to new independent EPC contractors when You can maintain your own single contract controller. In fact, such an EPC contractor is an internal division of the Customer’s financial and industrial group and mainly bears the coordination and dispatch load and the scope of authority within the classic capital construction department. The EPCM contractor is part of the Customer's structure and is practically deprived of entrepreneurial initiative as an independent subject of market activity.

- Nominal EPCM contractors are a separate class of ISP participants, sometimes very inconspicuous, but very important for understanding the functioning of the EPCM contracting market as a whole. Nominal EPSM contractors can be of 2 types:

- Operational is an enterprise or government agency that will subsequently operate the facility under construction. In this regard, it is easier for the Customer-Investor to attract such a potential controller in advance under a separate contract or due to the system of relations between government bodies to perform the functions of an EPCM contractor. Such a contractor most often does not act as a financial operator; he does not enter into contracts with lower-level contractors and designers, but bears the entire burden of responsibility for the construction schedule, commissioning dates, quality of work and their compliance with the project. Last but not least is their responsibility for achieving the set performance and power indicators (Fig. 2).

![]()

Rice. 2. Implementation of projects with the involvement of a nominal EPSM contractor.

- A technological or technical nominal EPCM contractor is needed when the Customer is not able to independently control the quality of construction or the quality of the object itself largely depends on the accuracy of compliance with the technological solution and is associated with complex and high-precision equipment. This applies to both chemical technologies and the construction of high and fine technology facilities, where the right to use patented technology is tied to a specific owner or licensor. In this case, an engineering company that has the necessary set of competencies to achieve the required quality of a commercial product is the best nominal EPCM contractor, since control over the accuracy and quality of the structure, the interaction of design and construction contractors, and, importantly, the compliance of the quality of the equipment with the required one depends on it process. In this case, contracts with specific performers and their payment are also made by the Customer, but not a single operation is carried out without the approval of the nominal EPSM contractor, although he does not bear real financial responsibility for the final result and does not take on the risks of failure to meet construction deadlines. The operation scheme is similar to that shown in Fig. 2 only with the amendment that this is the holder of “Know-How” or his representative.

- An independent EPSM contractor is the parent enterprise or management company of the EPC holding, the most widespread trend in engineering development today. Such a Contractor occupies an effective intermediate position between a pure EPC contractor in terms of price offer and an independent EPC contractor who does not own his own forces in principle. The main problem of contracts with management companies of EPC holdings is the internal relationship of the parent or management company, most often acting as a counterparty and financial accumulator, with the enterprises of the holding, since the ability to use accumulated preferences in tenders is not always combined with the effective manageability of a block of subsidiaries. Already today, a number of energy EPC holdings demonstrate a significant failure of controllability in the implementation of projects due to the lack of a coherent motivation system within the holding, which should become a significant factor for Customers when making decisions.

Consortium EPC/M contracting

It's no secret that the majority of modern EPC/M contractors grew up either from design organizations that decided to take control of supply and construction into their own hands, or from pure builders who acquired design and engineering departments. Or, finally, from suppliers of basic equipment, who only need to take over the management of the design and construction contract, leaving service and support for themselves in the future. To one degree or another, successfully, but such EPC/M contractors have made themselves known on the market: more successfully - the brainchild of large construction holdings, less successfully - with suppliers who managed to prove themselves on complex installations, even less successfully - with derivative companies from design organizations. The EPC/M contractors that emerged from them turned out to be the least adapted to the real management of construction projects. In response to the lack of EPC/M contractors as such or to the insufficient level of their readiness to implement complex projects, various types of associations, including consortia, have become a response, which have partially eliminated the shortage of competitors.

The consortium, as a temporary association of participants on the terms of a simple partnership, largely meets the conditions of the Customers, but always leaves some risks unresolved if they are not specified in the Consortium Agreements. This is especially true for the risks of joint liability when reasons for sanctions arise.

The disadvantage of this scheme is the inability to reflect the variability of the Consortium Leader, i.e. the participant with whom the customer directly enters into a contract. Typically, Consortium participants choose as a Leader or the most financially stable participant, ready to cover the entire range of warranty obligations, or a carrier of key consumer value for the Customer, whose services he simply cannot refuse. Such a leader may be a supplier of much-needed capital equipment that has monopoly rights to its distribution, service and warranties. On the other hand, the consortium EPC/M contractor absorbs and combines the problems of the EPC and EPCM models into a single contract mechanism.

Schematically, a consortium EPC/M contractor can be represented as in Fig. 3:

![]()

Rice. 3. Implementation of projects through consortium EPC/M-contract.

Possible options for dividing responsibilities within the consortium EPC/M contractor:

- Consortium leader - Supplier of main equipment. In this case, a construction and design management group must be formed within the Supplier, which will effectively interact with the relevant consortium participants. In essence, the formula of the classical EPSM model is transformed for this case into the format: P+EM+SM, i.e. The leader performs pure procurement and design and construction management. In this case, supplies only mean the provision of technological equipment; supplies of materials and structures remain with the general construction contractor.

- The leader of the consortium is an engineering company: the E+RM+SM model in relation to other participants. It is quite possible that the number of equipment suppliers is large and there is no point in including them all in the consortium, especially if it is based on a certain license for the technological process. In this case, the engineering leader of the consortium takes over the supply of equipment, leaving other supplies to the construction partner in the consortium, and the model is transformed into the EEP+SRSM format, where EP is the supply of equipment, CP is the supply of construction materials. It is quite possible that when building such associations, other intermediate forms of interaction may arise, but the main thing remains the transparency of the functioning of such a community for the customer and the clear distribution of risks between project participants;

- The leader of the consortium is a powerful local construction contractor, the most appropriate form for cases when technologies, equipment and construction resources of companies of different nationalities are combined within the framework of one large and complex project. In this case, the construction leader of the consortium forms a project management group that interacts with other consortium participants. It is likely that in the case of maximum proximity of the consortium EPC/M contractor to the EPC model, it creates a single project management headquarters from representatives of all participants, which performs the functions of a control module.

As already noted, consortium EPC/M contracting successfully unites and combines the advantages of the EPC and ERSM models, while allowing, through the mechanism of collective responsibility of participants, to implement serious projects. The flexibility of such associations serves as a kind of switch between EPC and EPC models, which, in conditions of price competition, can significantly affect the Customer’s choice. With all this, the most important point remains the Customer’s principled position in relation to the future brainchild. If the Customer is interested in maximum operational efficiency of the project in the future, which means he expects to have a significant influence on the project development process, then the announcement of a competition for the EPC contract may become a significant obstacle to the implementation of the project. It is in such cases, when the Customer’s position is as active as possible, that the EPSM model becomes a significant factor in the success of the project, since it assumes the possibility of forming the cost of the contract on the principle of “Costs plus the EPSM contractor’s remuneration.” And the opportunity to transfer all risks to the contractor may well be realized through convertible contracts.

Convertible forms of EPC/M contracts.

The conceptual dissonance that exists today between the theoretical principles of EPC/M-models and the practical implementation of contractual relations fully reflects the conflict of interests between the desire to fully control the project implementation process on the part of the Customer and, at the same time, minimize their risks and costs. The consensus in such negotiations may well be convertible contracts, which will successfully combine the Customer’s active position in participating in the design and the final transfer of risks to the general contractor for the implementation of the project as a whole. In essence, such contracts are a tool for the transition from the EPSM contract to the EPC model, which at the final stage is always more beneficial for Customers.

Of course, the Customer wants to have a higher degree of security regarding the main risks of the project, such as cost, timing and quality. That is why he tries to transfer maximum risks to the EPC/M contractor, even despite the higher cost compared to a contract for a conventional general construction contract. There is one more (fourth) main risk for the project owner, in addition to the three mentioned above, namely the risk of failure to meet the design parameters and performance of the process unit. It is the price-risk ratio in the EPC/M contract that is reflected in the choice of pricing model, which in general can be reduced to four main ones:

- Fixed price or “Contract by key” (Lump-sum or LSTK - Lump Sum Turn Key) is a standard option for EPC contracts, when all the risks lie with the Contractor, and the customer takes a frankly passive position in the selection of technical solutions during the design;

- Costs plus remuneration (Cost-reimbursable or Cost-plus-fee) is a standard option for EPSM contracts, when the Customer and Contractor share the design risk among themselves depending on the Customer’s activity;

- Unit Prices are one of the variants of the Open book methodology, when the Contractor determines its pricing based on the estimated cost of a man-hour for each employee, worker, machine-hour for each type of mechanism, reports on them and the Customer pays after the fact. This option is used at the stage when it is impossible to accurately estimate the amount of work;

- The pricing procedure is one of the Open book options, that is, when the contractor shows its pricing based on agreed upon estimated pricing methods in conjunction with the coverage of additional or actual costs not covered by the estimated standard prices.

Based on this simple classification of risks and pricing options, it is possible to create a 4X4 matrix of possible options (see Fig. 4) for the transfer of risks from the Customer to the Contractor in convertible EPC/M contracts according to various factors as a condition for the completion of one or another stage of the project.

![]()

Rice. 4. Matrix of distribution of typical risks for different EPC/M-contract schemes.

For example, in the case of a fixed contract price, the Customer prefers to cover all risks, but at the same time he must understand that he is automatically removed from influencing the choice of project solutions and gets what he has. Such a contract is of interest to a non-professional Customer in the field of design, or when the Contractor is subject to strict restrictions on the cost and technical parameters of the facility. Another option is when the parties use unit prices: the Customer can vary the scope of work, put forward his wishes, while the Contractor removes the risk of timing and the final price, retaining quality and production indicators. An option is possible when the price is formed using the “cost plus reward” algorithm. In this case, the Customer takes on the price risk, since in pursuit of the volume of remuneration, the contractor can artificially inflate the cost of design solutions and the corresponding estimates of such estimates, while the Customer leaves all other risks on the Contractor’s shoulders: the Customer receives quality, deadlines and productivity, and, in addition, it can objectively interfere with the development of the project.

Finally, a case is possible when the Customer, in fact, manages the design, makes technical and design decisions himself, and the contractor simply puts them on paper. In other words, the Customer bears the risk of price, timing and performance, and the Contractor bears only the risk of quality of work. This scheme is most likely for an active Customer who in the future plans to operate the facility on his own. This is especially clearly expressed in reconstruction, expansion, modernization and technological re-equipment projects, in which the Customer defines the requirements for the final result of the work professionally. It is in this case that the moment comes when, after agreeing on the last working drawing, the customer switches to the status of a passive observer and really wants the risks to fall on the contractor in full. In this case, convertible contracts become the best way out.

A convertible contract is one of the types of hybrid contracts in which the Customer and the EPC/M contractor take joint risks depending on the degree of project readiness and the Customer’s desire to participate in custom specifications and technical solutions. Therefore, at the stage of approval of the final project with the participation of the Customer, the convertible contract is implemented as a reimbursable contract on a cost-plus basis or on the basis of agreed unit prices for the volume of work, and upon completion of the design work it is converted into a fixed-price “Turnkey” contract and all the risks finally pass to the contractor. Thus, the Customer’s ability to transfer the risk to the contractor becomes realizable even in this case. However, negotiating a fixed price becomes a matter of bargaining at the stage of signing a convertible contract, and not of competitive selection, as would be the case in the case of a pure tender for an EPC/M contract.

Another advantage of a convertible contract is the ability to accelerate and carry out construction, supply and design work in parallel, which significantly reduces the overall construction time. After all, the EPC/M model itself appeared as a tool for accelerating project implementation, although this is not fully possible in all jurisdictions. If at the beginning of the negotiation process, even taking into account the fact that the Contractor won the contract in a competitive competition, there is no unequivocal approval of its individual technical solutions by the Customer, a convertible contract will already allow work to begin, and minor approvals to be carried out in a working order.

In general, you can consider the following options for convertible contracts, depending on the initial and final purpose of contracting:

1. From given (specific) prices per unit of power to a fixed price. It assumes that, based on the results of the tender selection, the winner proposed the minimum contract value in relation to production capacity (per 1 MW, per ton of product, per unit of product, etc.) based on a specific technical solution. The customer reserves the right to adjust technical solutions, but the balance of discrepancies in one direction or another is reflected in the specific price upon making the final decision. At the same time, the initial price allows you to start pre-paying the project, purchasing resources unrelated to technical solutions and other work.

2. From the EPC pricing model (costs plus remuneration) to the EPC model with a fixed turnkey price. Such a contract has the right to exist if, at the initial stage, the Customer personally carries out work to select technology and equipment for future production, the cost of which cannot be included in the fixed price initially. In this case, the Contractor first carries out the work as a consultant on the basis of an agreed remuneration, but after the main components of the technological process have been selected, he prepares a fixed price for the design and completion of construction and installation work.

3. Any of the options for transition from open pricing to a fixed turnkey price (Open Book with conversion to LSTK), for example, from unit prices to a fixed price. It is used in cases where production capacity, and therefore the volume of work, largely depends on the wishes of the Customer, and when the final volume is determined, it is possible to switch to a fixed contract price, taking into account all risks.

4. Another option for a convertible contract may be the option of transitioning from the implementation of individual volumes of work to the construction of an entire facility. Its difference from the previous option is that the cost of the contract is formed as the design of individual buildings and structures of the project is completed. At the same time, the Customer does not have firm confidence that he is ready to finance the entire project at once. Therefore, construction is carried out according to launch complexes, stages, queues or other technological groups, which entails a change in price. But after the entire project is completed, switching to a fixed price is quite justified.

A natural disadvantage of such a contract is the possibility of changing prices over time or indexing costs according to estimated pricing, which will become a natural stumbling point when the Customer delays decisions. On the other hand, the effect of production scale can play a significant role, when the volume of deviations in the Customer’s wishes significantly affects the calculation of initial prices. All these subtleties must be discussed at the stage of signing a convertible contract, up to the gradation and classification of such deviations according to various factors.

And finally, an important factor in the convertibility of the contract may be a change in the contract procedure for payment for work performed. As you know, all payment methods can be grouped into the main ones:

- Payment after completion of all work or complete payment (Payment after completion);

- Payment for completed structures or start-up complexes (Milestone payments);

- Payment according to the construction schedule (Progress or Scheduled payments);

- Payment based on the actual volume of work performed in the reporting period.

All of these payment options are initially comparable to a specific pricing model and are most acceptable at a specific stage of the work. At the same time, as the design work is completed, the cost of equipment and logistics surcharges are agreed upon, the flow of advance payments and repayment schedules are finalized, and the amount of guarantee deductions is agreed upon, a transition from more risky payment methods to less risky ones for the Customer is quite likely. In this process, it is quite reasonable to take into account the contractor’s additional costs for attracting working resources, which will definitely increase the fixed price, but will allow the customer to more accurately plan the indicators of the business plan.

As you can see, the use of EPC/M models in their pure form is either impossible in practice or requires a clear and detailed analysis of the specific conditions of applicability for the implementation of a specific investment project. And the possibility of a flexible approach to planned changes in contract terms during the execution of work can make such projects more transparent and balanced with regard to risks and relationships between the parties. In any case, this should be taken into account by Customers and Contractors before signing contracts.

OK- inform continues a series of publications about the current situation in Russian construction. The construction industry is a recognized “locomotive” of the state’s economic development, but the builders themselves say that this locomotive can easily end up in a sump on a siding. If systemic measures are not taken today to bring the construction industry out of “stagnation,” we will soon have to talk about real programs for its restoration, says our interlocutor today, the general director of an industrial development company in the oil industry, an expert consultant in the field of investment management. construction projects Vladimir Ivanovich Malakhov.

Vladimir Ivanovich, how do you assess the current state of the construction market in Russia, and what do you see as the main trends and directions of its development in the coming years?

How contradictory and unstable. On the one hand, we have quite large and even growing volumes of capital construction in the country in recent years, from 3-4 to 6-7 trillion rubles, on the other hand, there is a humiliatingly unsystematic state of the construction industry as a whole, with no real prospects for its qualitative change. The very fact of such volumes of construction should mean that the industry has tremendous opportunities to make an almost quantum leap forward, both in technology and in the resource base. But instead we have to note the ongoing stagnation of the construction cluster. This applies to personnel training, the use of advanced technologies in construction, and the use of the best project management tools. Moreover, I am sure that soon we will have to talk about real programs for the development and restoration of the construction industry.

And here there is no point in referring to crises. Despite the fact that the construction industry, due to the inertia of its economic mechanism, was the last to feel the consequences of the crisis, it still significantly hit development companies. At the same time, the total volumes of construction production almost did not decrease due to the presence of both large-scale government projects (such as the APEC Far Eastern Summit, Sochi Olympics, Kazan Universiade, etc.) and large corporate programs of Gazprom, Transneft, Rosneft, Rosatom, Rostelecom and others players in the commodity and energy sectors, which are not so easy to cancel or suspend. In a certain sense, here lies the contradiction - these projects, on the one hand, save our construction industry, on the other, they destroy it.

But still, the main reasons for the disconsolate position of the industry, in my opinion, are not related to crises. Rather, it is the low quality of public administration and regulation, including through the SRO system, and growing corruption. Imperfect legislation on public procurement, manual management of large infrastructure projects through affiliated contractors and the lack of basic planning, no matter how funny it may sound in a market economy, also contribute.

Can you speak a little more about these reasons? What ways out of this situation can be considered?

Let's try it in order. First, self-regulation. I think there is no need to prove to anyone that the creation of the SRO system in construction not only did not live up to anyone’s hopes, but confidently demonstrated the complete fallacy of the basic concept and the semantic paradigm of its existence. Self-regulation today has completely degenerated into funds for collecting money and ineptly managing contracting companies in order to increase fundraising. Managers do not yet have any other goals for self-regulation.

The goal of self-regulation in construction was initially correct - to create an institution to formulate the rules of the game in the market, which, in essence, provides a legal opportunity for the contracting sector to agree on achieving common interests, including those affecting clients. Such interests include both the creation of a unified regulatory and technical base for construction and regulation of activities in construction, and the creation of tools for protecting the rights and interests of builders before government agencies, customers and the market. Now let's think: can 200-300 self-regulatory organizations create some kind of unified regulatory framework, and even generate new requirements and rules in the market? Of course not! All communication with SROs among builders today comes down to paying dues and avoiding persecution of negligent people. At the same time, the state transferred part of the functions of licensing and monitoring the competencies of market participants to SROs. But if these are government functions, why should the construction sector pay for them a second time out of its own pocket, since it already pays taxes to carry out government tasks?

- Can’t self-regulation in construction play a positive role?

We need to look at the situation from the market point of view: SRO should be an institution that provides contractors with clearly greater benefits and opportunities from participating in it than without it. Starting, for example, from joint defense of construction companies in courts to insurance of force majeure risks. An SRO may well insure the risks of damage to third parties if the cause of the insured event was the lack of knowledge of some processes or an unforeseen change in the original design conditions. In other words, risks that arise during the construction of a facility, but which cannot be unambiguously attributed to a specific person.

This is why an SRO system is needed, then every contractor and his owner will have peace of mind even after retirement and the closure of his company. In addition, if a SRO participant can get access to any consultations and materials, and his competitor without an SRO will be forced to buy all this documents from a single standardization center, then the benefits will become more tangible in material terms. In other words, if SROs begin to perform some of the generally accepted tasks of the Chamber of Commerce and Industry in construction, then this can play a significant role in the formation of civilized small and medium-sized businesses in construction.

- What to do about corruption and the imperfection of the law on public procurement as it relates to builders?

Thousands of copies have already been broken on this occasion. It is unlikely that I will say anything new in terms of criticism of the very concept of public procurement. The laws seem to be improving, but corruption remains the same and is even increasing. Officials are coming up with new ways to ensure victory for their affiliated companies, and if this is impossible, they spoil the lives of those who won, until the winning contractor is replaced by their own accountable company, spoiling it to such an extent that third-party participants willy-nilly become unscrupulous performers. This often applies even to companies appointed “from above,” since lower-level officials do everything to ensure victory only for their entrepreneurial partners in budget development...

One government customer – one contract.

I believe that the introduction of just a few rules regarding the concept of public procurement can significantly reduce the corruption component:

First: the company that wins the tender cannot enter into new tenders with one specific government customer until the signed contract is fully executed. The principle is called: One government customer – one contract. No one prohibits other government customers from participating in tenders, but if a unified register of government contractors is subsequently created, then another customer will be able to use it to track the state of affairs on other government contracts and make appropriate decisions. This principle makes it possible for new companies to enter new tenders. The interest to return to their customer will force contractors to work better and, most importantly, faster. This leads to both lower overhead costs and competition for resources. And most importantly, knowing that there can only be one contract, strong companies will fight for the largest contracts in terms of capital investment volumes, leaving small contracts to small and medium-sized businesses. Isn't this government support for small businesses? This is exactly what builders expect from the state. Of course, there will be hundreds of arguments against such a rule, ranging from the lack of a sufficient number of contractors to the lack of contractors with the necessary resource and technical readiness. But these are all technical details that can be written down based on an analysis of the retrospective of contracts and the state of the markets.

The contract price is not a factor in determining the winner.

The second rule can be stated simply: The contract price is not a factor in determining the winner. To select a winner, very specific parameters or indicators must be assigned, based on the totality of which the winner is determined automatically, i.e. almost like a computer. Why can't you focus on price? Because there will always be companies that, including purposefully, by conspiracy, in order to eliminate competitors, will engage in dumping. In some contracts, dumping reaches 50%. What kind of competitions are these? Anyone, even a young specialist in construction economics, will tell you that this is impossible. Everyone understands that dumping of 30-40% is either the result of unqualified calculations or fraud of bidders... By stopping price competition, the connection between affiliated customers and contractors can be broken and, perhaps, real competition for quality and deadlines will finally appear. Stopping price competition will require solving the problem of adequately calculating the starting competitive price, and this is an issue that can be easily and clearly resolved.

Determining the selection of the winner should be such indicators as the “collateral protection coefficient of the government contract” (the ratio of the value of the company’s real estate to the amount of the contract at the time of filing the application) or the “liquidity ratio of the government contract” (the ratio of the company’s own working capital to the total portfolio of orders at the time of filing the application ). We can give a few more examples, but the main thing is that government orders should be received by companies with guarantees and own capital, then the level of responsibility for the results of the work of the owners will increase significantly.

- You also mentioned the pricing system, what can be done in this area?

The last rule concerns the pricing system. Today there is a lot of criticism of estimated pricing in Russia, although this only confirms the harsh truth about the disqualification of our management personnel. Estimated pricing is just a way of calculating the cost of work; it is based on laws and rules that we ourselves approve, so calling it backward or incorrect is at least ridiculous. The main thing is to understand that at the stage of the competition it is possible to calculate the value of the contract using more integral tariffs and estimates, consolidated or given unit prices, and at the stage of drawing up working documentation, of course, to operate with more accurate prices and volumes. The main thing in this is the ratio of the final cost of the contract to the contractor. Indeed, today the difference between the price of the general contractor and the final contractor can differ significantly. But they are considered according to uniform reference books and rules. The whole secret is in the subsequent undressing of the real performers by the owners of the first contract. Therefore, the rule here is simple: The estimated cost is the cost of the work of the last performer.

The estimated cost is the cost of the work of the last performer.

What does this rule mean? This means that the price is compiled only for the company that directly performs the work, with shovels and equipment. The law should establish that this last performer should not receive less than this estimate, either in wages or in covering other expenses. All other services, for example, general contracting, must be calculated using a separate coefficient and, accordingly, paid. Where it leads? First of all, this will force general contracting companies to compete on the cost of general contracting services, rather than construction work determined by the estimate. Reducing the cost of these services will be possible if such companies perform only part of the construction and installation work on their own. Or they will reduce the cost of maintaining the management apparatus. Indeed, today there is a complete imbalance in the pricing of low-level subcontracting. The general contractor, most often an affiliate of the Customer, takes the maximum share of the revenue margin, leaving the subcontract on a starvation diet. Hence the low quality of work, unprofessional staff and other problems. If the general contractor is obliged to pay down the entire estimate by law, then qualified personnel will go into line contracting, and there will be an opportunity for further development and competition. In addition, the very creation of a provision on assessing the cost of the services of a general contractor, EPC or ERSM contractor will allow competition specifically for these services, and not just for everything in bulk. And their profit should be included in the cost of these services, and not taken away from the last performer.